Cars, houses, Facebook and stagnant incomes – why you’re so stressed about money

ROB CARRICK PERSONAL FINANCE COLUMNIST – GLOBE AND MAIL – March 8, 2019

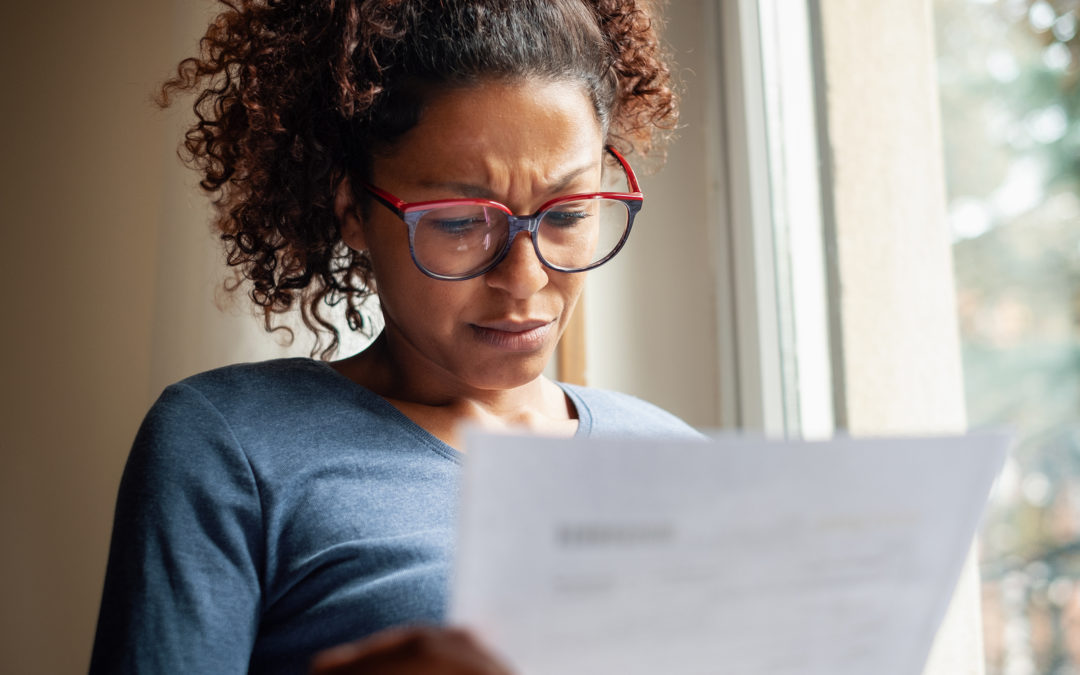

Philip Bailey is worried that the family's cost of daily living is making it difficult to save enough for retirement.

A lot has gone right for the economy in the past decade, yet evidence is mounting that Canadians are worried sick about money.

People are losing sleep over their household finances and their physical and emotional health is suffering. “I keep Kleenex in my office all the time,” said Shannon Lee Simmons, a financial planner in Toronto whose clients typically come in to talk about things such as the soaring cost of housing, crippling debt levels and an inability to save for retirement. “People cry often.”

Financially speaking, Canada has been one of world’s most fortunate countries since the Great Recession. We’ve had low interest rates, strong house-price gains in many cities and enough economic growth to drive the unemployment rate to extreme lows without igniting inflation. Statistics Canada said on Friday the country has seen the creation of 369,000 jobs in the past 12 months, including 266,000 full-time jobs.

In economic terms, these are good times. Yet, a recent study by the analysis firm Seymour Consulting found that nearly half of people lose sleep at night as a result of concern about their finances and almost four in 10 people believe money worries are affecting their health.

Rami El Mawed, a 33-year-old engineering intern in Thunder Bay, is stressed about having to pay hundreds of dollars every month to get out from under his line of credit and credit- card debts. He worries that he would have nothing to fall back on in an emergency such as losing his job. “I never have extra cash to put into saving," he said.

Philip Bailey, a 45-year-old environmental consultant in Vancouver, said he’s worried that the cost of daily living for his family of four is preventing him from saving enough for retirement. “If I were to take that ‘Wealthy Barber’ approach of paying yourself first and do it properly, then we would be right on the edge,” he said. “I think we’d be eating into our emergency reserves if we were really paying ourselves first.”

A survey commissioned by the Canadian Payroll Association last month asked just more than 1,000 people to rank the following common life stresses: Money, personal health, work/career, too little time, political and social issues, dependants (kids, elderly parents) and marriage/divorce. Money stress dominated. Almost 40 per cent ranked it as being most stressful, compared with 9 per cent for second-ranked personal health and 8 per cent for third-ranked work/career.

Seymour Consulting has found that money stress leads to a feeling of powerlessness – a sort of money shame that people keep private. But financial stress could become a public discussion in the federal election campaign coming this fall.

The federal Liberals won the 2015 election on a platform that emphasized help for the middle class and inclusive growth. After taking office, the government lowered taxes for middle earners and introduced a revamped child benefit that has been credited with helping to lower the poverty rate for children. But it may be difficult for the Liberals to brand themselves as champions of the middle class in this year’s election when so many people are so worried about their finances.

Aside from flashes of trouble in provinces affected by declines in oil prices, money stress just starting to show up in the economy. The credit-monitoring firm Equifax Canada has reported a small increase in the number of people falling behind in paying mortgages and other kinds of debt in the final three months of 2018. Equifax noted that consumer bankruptcies have also been increasing.

These increases are coming off historically low delinquency rates, though. “Mortgage [delinquency] rates in particular are at remarkably low levels,” said Bill Johnston, vice- president of data and analytics at Equifax Canada.

Mr. Johnston said delinquency rates are closely connected to the unemployment rate, which hit a 43-year low of 5.6 per cent at the end of last year and now sits at 5.8 per cent. Economic growth did slow in the final three months of 2018, so the jobless rate could rise.

This same weak economic growth trend reinforces another key economic support: low interest rates. Rates have mostly been rising since mid-2017, making mortgages, loans and credit lines more expensive. Undoubtedly, this has contributed to financial stress levels and delinquencies on debt payment. But rates are still low on a historical basis and unlikely to rise unless inflation, as measured by Statistics Canada’s consumer price index, becomes a problem in the mind of the economy’s maestros at the Bank of Canada.

But while official inflation figures remain low at less than 2 per cent, the cost of living as perceived by families is another matter. It’s one of the biggest factors in trying to understand household money stress.

“I find groceries cripplingly expensive in this city,” said Mr. Bailey, the Vancouverite. “And buying stuff for the kids.” Mr. Bailey feels that the solution to their financial squeeze has to be 'a lifestyle change on my family's part.'

He and his spouse have children ages 3 and 5, with combined monthly child-care costs of $1,630. Camps to provide care during the summer and at spring break add another $2,500 in costs each year, and sports and arts activities add another $1,000.

Mr. Bailey and his family live fairly modestly despite their comfortably middle-class income. They have one car, they live in a three-bedroom townhouse and their restaurant spending is limited to takeout once a week. Yet, he has talked to his wife about selling the car and travelling less to visit parents in London, Ont., and near London, England. “If anything will fix this, it needs to be a lifestyle change on my family’s part.”

Changing lifestyle expectations have put families such as Mr. Bailey’s in a tougher position than earlier generations. Smartphones and their data packages can add a couple of hundred dollars a month to household spending, and so can a new generation of activities for kids, such as competitive dance and after-school math-tutoring programs.

Rising incomes can help families feel more in control of their finances. But one of today’s big economic disappointments is that the low unemployment rate has failed to produce meaningful wage growth.

Armine Yalnizyan, an economist and policy adviser at Employment and Social Development Canada, said median wage growth was below the inflation rate last year and has, in fact, been slowing since the financial crisis. Her theory is that wage growth is being squeezed by employers who are coping with today’s modest level of economic growth by clamping down on costs such as worker pay. “That’s not great for the average working-age household’s ability to purchase more,” she said.

Weak income growth has not stopped people from borrowing steadily more in recent years through lines of credit, mortgages, loans and credit cards, although the rate of growth has slowed. Canada actually needs consumers to borrow and spend. According to Ms. Yalnizyan, 57 per cent of economic output depends on household consumption of goods and services.

The low delinquency rates on debt repayment suggest borrowing has not reached toxic levels. Yet, debt is a big driver of financial stress.

Mr. El Mawed, the engineering intern in Thunder Bay, came to Canada from Lebanon in 2006 and managed to graduate without student debt thanks to help from his parents. But he found himself relying on credit cards and a line of credit to afford other costs, including a car.

With the help of personal-finance blogs and books, notably Tony Robbins’s Money: Master the Game, Mr. El Mawed was able to draft a plan to pay his debts in two years. Now, he worries about a lack of savings for emergencies and long-term goals such as owning a house.

“It’s constantly on my mind,” he said. “I’ve been wanting to buy a house – in Thunder Bay, it’s quite cheap. You can buy a house for $180,000 and it’s in very good shape. But I simply have no cash flow by the end of the month. I know I’m paying too much towards my debt.”

Financial stress is hardly a new phenomenon. In the 1980s, there was a recession, rampant inflation and mortgage rates around 20 per cent; the 1990s began with a severe recession and job-killing corporate restructurings; in the 2000s, there was the tech crash, 9/11 and a global financial crisis. Common to these and all other decades is the unavoidable precariousness of balancing the cost of a mortgage and raising children with extras such as owning a car or two, travel and home upkeep.

Today’s financial stress seems different, and not just because of the lack of any major problems in the national economy. For one thing, there are more ways to accumulate debt.

“In the old days, people came in to see me and they had a bunch of credit-card debt,” said Doug Hoyes, a licensed insolvency trustee with Hoyes Michalos. “Now, they still have credit- card debt, but they also have a line of credit.”

Mr. Hoyes also sees many more people using debt to cover living expenses than he did 10 years ago. This view is backed up by a Financial Consumer Agency of Canada report showing that about one-third of people with a home equity line of credit, or HELOC, used it to cover day-to-day expenses and/or emergencies.

People also owe more than they used to, both when measured against incomes and by pure dollar value, Mr. Hoyes said. The ratio of household debt to disposable income was almost 178 per cent in the latter part of last year, double the level of the mid-1990s. The credit- monitoring firm TransUnion says the average non-mortgage consumer debt load at the end of last year was $30,257, up 22 per cent since 2011.

Precarious work, optimistically branded as the gig economy, is another new stresser for household finances. A Canadian Centre for Policy Alternatives study from last year included survey results indicating that 22 per cent of professionals in this country work on a part- time, contract or freelance basis and thus probably lack a pension or benefits to help pay expenses such as dental work or glasses.

John Goranson, a university instructor in Victoria, has been working contract positions since 2002. He’s worked in five Canadian cities as well as abroad and never had a pension other than one offered by an employer in South Korea (he took the cash when he left the country).

“I earn almost the same now at age 45 as at 30 because pay in my industry hasn’t risen and the work I do is basically the same as 15 years ago,” he said by e-mail. “The only way to boost earnings is to work more, but obviously that isn’t sustainable.”

Rob Carrick asked his Twitter followers for household expenses that didn't exist 20 years ago. Here's what they said.

The high cost of housing is a glaring example of how financial stress is different today. An old rule of personal finance says a house should cost no more than three times your household income. Average Toronto prices were an estimated nine times median household income at the end of last year, while Vancouver prices were 13 times higher.

John Pasalis, president of the real estate brokerage Realosophy Realty, said too many people buy houses today without thinking about how they will afford not only their mortgages, but future costs such as daycare, car loans and renovations. “What I’ve been thinking over the past few years is that a lot of people’s financial stress is probably rooted in bad real estate decisions,” he said.

The same might be said of car-buying, specifically the shift away from cars and into pricier SUVs. The market research firm J.D. Power says cars last year represented 27 per cent of retail vehicle sales, down from 42 per cent in 2014.

A demonstration of the SUV-car price gap: J.D. Power said the cost of a Honda CRV is a $10,000 step up from a Honda Civic, which is built on the same platform as the CRV. This price gap helps explains why the monthly payments on new vehicle loans are higher and last longer than they used to.

J.D. Power numbers show the average car-loan payment was $666 a month early this year, up $100 from 2015. Just over half of new vehicle loans have terms of 84 months or longer.

“Canadians are choosing to spend more,” said Robert Karwel, senior manager of the automotive division for J.D. Power in Canada. “And they’re allowed to do that because of the financial instruments available like long-term financing.”

Social media adds to financial stress as it amplifies the urge to have what others have and live how they live. The rise of the internet and social media may also help explain why financial stress is so prevalent today and different from what we’ve seen before. One way of explaining our consumer society is to see it as built, in part, on imitating others – we desire what we see others are buying and doing. Social media and the internet amplify this condition.

To start with, people are seeing more ads than they did before. David Soberman, a professor of marketing at University of Toronto’s Rotman School of Management, said the number of ads people see each day was as many as 200 back when he started teaching in the 1990s. Today, various studies estimate people see 1,500 or 2,000 a day.

Almost everyone who studies financial stress agrees that social media and Facebook are an aggravating factor. “When you’re on Facebook, people are always posting about the great things they’re doing,” Prof. Soberman said. “When you see this, you say, ‘I’m not doing that,’ and that creates stress for you.

“We didn’t use to see that,” Prof. Soberman adds. “You used to find out over time, when you were having a beer with someone two years later.”

Overspending leads to debt, which gives people anxiety about their finances. But not spending can be stressful, too.

Ms. Simmons, the financial planner, says she and her husband consciously chose to control their spending by living in a small two-bedroom home in Toronto and, until recently, driving a 2008 Jetta with more than 200,000 kilometres on the odometer. They now own a used minivan.

“I see how much stress overspending can put on families and I don’t want that for my family,” she said. “As a result, I end up living well within my means. The cost of that, where the stress comes in, is sometimes a sinking sense of inadequacy.”

Financial planner Shannon Lee Simmons and her husband made the conscious choice to live within their means, but she says the cost of that is 'a sinking sense of inadequacy.'

Ms. Simmons said it’s wrong to call people vain or shallow for wanting to drive a nicer car or own a bigger house. “I think it’s about fitting in and not feeling that you’re falling behind.”

The workplace is where the effects of financial stress are most noticed and discussed. Jillian Kennedy, head of defined contribution and financial wellness in Canada for the consulting firm Mercer, said employees distracted by their money worries may not work as productively or call in sick, and they can negatively affect co-workers.

Ms. Kennedy uses the example of a money-stressed manager whose job it is to acclimatize new employees to a company. “Imagine how this spills into the organization,” she said. “That person affects their team and their peers as well as people being hired. It’s a huge problem that is just starting to be talked about.”

Mercer’s research shows that women on average are more worried about money than men, and that higher income levels don’t insulate people from money stress. Households with more than $100,000 in income were just as stressed about paying bills and saving for retirement as those with lower incomes. There may even be additional stress for high earners because they’re looked upon as leaders and mentors.

Another insight from Mercer’s research is that people can be financially literate and still suffer from money stress. This explains why some employers and groups involved in financial education are focusing more on financial wellness and less on financial-literacy basics.

Mercer says there are four elements to financial wellness, which are:

- Control over daily and monthly finances: Do people know how much money is coming in and going out, and are they comfortable with it?

- The ability to absorb a financial shock: a sudden expense of $500, for example;

- Making progress toward financial goals: retirement, but also short-term goals such as home renovations;

- Financial freedom: Do people have the money to travel or retire when they want?

A company called BestLifeRewarded Innovations says it has reduced employee overall stress levels by 19 per cent over 12 months with online wellness tools that help people monitor their stress and make small changes in lifestyle or habits. These tools, including educational content, quizzes and a budgeting tracker, are offered through insurance companies that incorporate them into workplace health benefit plans.

In the order of urgency of their situation, people worried about money can consult financial planners, non-profit debt counselling agencies and insolvency experts. With planners, look for accreditation such as the Certified Financial Planner (CFP) or Registered Financial Planner (RFP). Many planners are compensated by selling investments, but a growing number offer advice for an hourly or flat rate.

The risks posed by high levels of financial stress go well beyond distracted employees and their worried bosses. U.S. research shows people who report low levels of financial well- being exercise less, smoke more and are more likely to experience depression and obesity.

Feeling anxiety about their financial position can also make people resentful and angry, said Jose Jaime Guerrero, a counsellor and financial coach in Burnaby, B.C. “You can see the divisions between people in the United States are a reflection of that.”

The coming federal election will be an opportunity to test the mood of financially stressed Canadians and see what they expect of politicians. One way for governments to help would be to ease the burden of daycare costs either directly or through subsidies or tax breaks for parents. There’s also pressure on the government to help first-time buyers who are priced out of the housing market.

Shachi Kurl, executive director at Angus Reid Institute, said the 2017 B.C. provincial election offers a glimpse of how things could go if financial stress isn’t acknowledged in some way by politicians. The B.C. economy was, and remains, one of the country’s strongest. Still, the ruling Liberals were voted out.

Ms. Kurl believes it’s because they failed to acknowledge that a significant number of voters were feeling uneasy about their financial well-being. “Just because the economic fundamentals are good, it doesn’t mean everyone is feeling it.”

© Copyright 201 The Globe and Mail Inc. All rights reserved.